The power of a good business book, lies in how you put its lessons into action!

Business books. Powerful tools if used to their full potential.

They can help us level up in life. But, they need to treated as educational books.

Read not only for pleasure but also with a strategy used to get the most out of them. I learn best by reading and doing, so this set of steps is key for me.

Here are 5 steps that I have learned from senior business leaders. These make sure you get the most out of the books you read.

Read the book more than once

In the same way, you would read a textbook. If you only ever read a business book once. You would miss a lot of detail. Which is where the deep lessons come from.

Me, I’ll read a book 2–3 times before I’m happy that I got the context from it.

The first read will be like any other book, I’m reading for enjoyment. I may add stick note markers in this first read.

In the second and third passes of the book, they are essentials tools for me.

Which brings us onto.

2. Note mark the book

I use the sticky thin colored marks but use whatever you have or whatever works best for you. At this stage, I’m marking out pages or lines that interest me. Those that I have more to learn from.

Those sections of the book ill go into much deeper detail later on.

Which brings us onto.

3. Take detailed notes

Each of those things I bookmarked?

As I go through my second and third passes of the book. I’ll be taking detailed notes on each of those sections and how they apply to me or my situation.

I’m looking at:

How does this lesson apply to me or my situation

What action can I take away from this

How do I take that action and take it into my day to day business

I will often fill a notebook during this process. That notebook stays with the book afterward.

Yes, most of my reading and evaluation is done while traveling. My laptop is huge so I don’t get much done in coach. I work on this instead.

4. A 90-day action plan

The actions I noted down in my notebook earlier?

Well, I have to hold myself accountable to put them in place. That means an action plan.

I give myself no more than 90 days to put them in action and review them.

For example, I give is standing meetings — this idea I was able to put in place the next day.

Others like something that affects culture or how we do business?

Well those take longer to put in place and review, so they take the 90 days.

Regardless of the timeline, because I have a plan and a set of actionable steps. I have something to hold me accountable to myself.

Action plans really do work, on so many levels.

5. I review the top 3 books in my collection often

The top 3 changes. They make the list based on how impactful they have been for me.

Those books, I revisit once a year. More if needed. Often if I have a problem I can refer to those books for some insight.

Learning by reading works for me. This is why having a strategy around my reading is key.

Final Thoughts

These books as I said can help us level up. They are also great for helping us to work problems through.

The best way to learn from the material and the insights is to have a strategy. That and actions you can be accountable for.

This is what works for me and others. I hope it is also helpful for you as well.

This for me is a game changer for a number of reasons and a lesson in what real business leadership should be in the 21st century.

Open and honest communication

Sharing the true detail of the situation

Giving bad news early

Transparancy on job losses

Tools for those leaving the company

All of these details were provided in this simple communication to the workforce.

Is their new CEO raising the bar in terms of how leaders treat their employees?

Too often we are kept in the dark, change comes fast and it’s often unexpected.

In this case, a whole bunch of changes, some positive, a lot more negative are going to hit BP employee’s.

The difference here is they know about them and can prepare.

That’s leadership and guidance in action.

We are all in this together….

Like all industries the energy industry is being hammered right now and BP are no different to any other company in this sector.

The difference here is that their leader, is making very clear in a simple and concise way the situation, the costs and what is going to be done.

Change is coming but its coming to us all and here is the timeframe for that change.

I can’t help but find this such a refreshing and different communication style that I really want to engage with it and share it.

Financial Direction

The energy industry typically pays bonuses and shares as part of the full financial package they offer to employees.

Being humans, most who receive the bonus spend it long before its in their pocket.

At the end of the year when despite making the targets those perks don’t come, the disappointment and sometimes the personal implications of that are very real.

Again the message was simple and concise, the bonus wont be paid so don’t figure it into your financial plans.

The disappointment may be real now, but there is time for employee’s to prepare themselves emotionally and in the real world for the fact its not coming.

That honesty to me is refreshing and powerful.

Not everyone will be sticking around

This wont be news to any of the employees in BP, they will know that job losses have to happen in order for that business to start making money again.

Too often though there is very little communication on these type of changes.

Here the organization has been told, what’s happening and why, the numbers affected and the timeline.

The news also extends to the help that those affected will get directly from the company as they make the transition into what will be an uncertain future.

Again very clear and concisely shared information with everyone.

The hardship will end…

Annual pay rise, promotions, flexibility these all will come back and more this year.

Timelines are shared, giving those that remain the comfort that while things are tough now, that will end and things will get better.

Takeaways?

This for me is a big change in how information is shared openly and honestly from the top down.

Employees have of course always known that they could be trusted with this kind of information, it breeds loyalty to the company and a true sense that we are all in this mess together and will come out the other side all the stronger for the shared experiance.

The type of leadership emerging in 2020 feel different, more engaging and with an honestly and open ness that’s not been there before.

That’s true in business with this type of emerging leadership style and also in politics I think with Jacinda Ardern in New Zealand for example (Although please see free to correct me on that if im wrong).

This is more than leading by example, its leading with a transparent set of actions and priorities that the public as well as your employees can hold you accountable to.

Whether it lasts or grows in momentum who knows?

What I do know how ever is that this is something new, we haven’t seen before, im both impressed and ready to see where this goes.

Success or failure its very much management and leadership in the public eye.

Could the gift of financial literacy be the greatest gift you ever give yourself?

There is some evidence to suggest that yes, it really could be.

Very few of us are fortunate enough to have financial literacy taught to us at school. As I wrote earlier in the week its a problem and we need to do more to support children and young adults to develop financial literacy at a young age.

What about us, the adults that didn’t receive that education? Well the good news is that there are plenty of resources our there to educate ourselves with.

Even those of us who have a higher education and studied accounting, finance or economics at a college or university level may not have a good grounding in financial literacy.

As the financial world becomes more complicated with things like cryptocurrencies being traded, banking moved online, and credit becoming harder to find as the financial institutions have struggled to fully rebuild since the 2008 financial crash, whilst at the same time being regulated more stringently.

Ive written before elsewhere about the millennials becoming a lost generation or the so called generation rent. The first generation in living memory to have a forecast lower quality of life financially than their parents.

Its frightening to think that this is a reality in the 21st century and for sure there are lots of different components to that which play their part such as:

Record low interest rates which have continued to fall since 2008, meaning our savings don’t accumulate as much interest as they used and so are worth less over the longer term

Inflation is running 2 -3% above interest rates so year on year, currency in real terms is worth less

Salary increases are not keeping with inflation in a lot of cases, so while the cash value of our salary increases every year, the real time value of that money is less that it was the year before. (Example is inflation is 3% and your salary increase is 2%, your salary is worth 1% less than it was the year before).

Mortgages require a higher deposit typically 15 to 20% which is difficult for many to achieve as they are in the rental system which leaves them with less cash to spend.

All of these points and more are making it harder for people to either get out of the debt that they are in, or to get themselves onto the property ladder, and this is where learning to be financially literate comes into its own, as a great gift to yourself.

So what is financial literacy anyway?

At its most basic financial literacy is the ability to understand our own financial positions and to have the ability to create a budget and financial plan to meet our goals. It should also include a very basic understanding of how financial products like debt work and what is to be avoided and why.

Its these basics which we will talk about today in this article.

The more advanced topics like, investments, financial products, leveraging debt to invest in real estate or a business we will leave for another time.

Back to basics with a budget

o you know what you spend each month? Not what you think you spend, but what you ACTUALLY spend!

I’d bet that a lot of us don’t, and that if you really looked it, you would be shocked at what you spend and surprised at what you could save.

This can all be determined with a budget, which is basically a spreadsheet with what’s coming into your bank account i.e your income on one side, and what’s going out i.e your bills and other spending on the other side like the example below:

This is what most us who wonder where their hard earned cash goes every month would see if they did a budget I know I did. As you can see a simple spreadsheet really works well to highlight what your spending and where. I normally use a 3 month average of my spending habits when I review my budget, all this information is available through your bank statement or digital banking.

As you can see the problem really is that in this example im stuck in a loop, im not getting into more debt, but im not getting out of the debt that im in any quicker and I have zero left over for saving.

If I took action based on what I see in my budget for example and made my own coffee in the morning, took homemade lunch to work and cut my eating out and nightsout budget by 30% each, then all of a sudden my financial situation looks alot better:

Suddenly I have $750 of spare cash left over each month, that I can use to claim back my financial freedom.

At its most basic this is financial literacy, being able to break down your income and your spending to work out what your outgoings are and what your financial position is based on those.

If using a spreadsheet and spending time on a computer to do all this seems a bit too much, an old fashioned pen and paper also works. Your bank may also offer you an app style resource in your digital or mobile banking apps and of course in the android and IOS app stores there are multiple budgeting apps to choose from.

Ok so now what?

Ok so now what?

This is the not so glamorous part, once we have the budget figured out and a plan for how we create some breathing room for ourselves, by having a surplus of cash each month, we need to figure out what to do with that (Clue I’m not going to suggest spending it living the high life just yet).

Really there are 2 options here:

Pay down debt

Save

Actually in an ideal world we would look to do both but it depends on the circumstances.

The first step is to look at your debt and work out how much interest you pay on it, or in other words how you much you pay back on top of the money you borrowed.

The higher the cost of the debt, the more we want to direct our resources to it, for example credit card debt normally falls into the category.

In our budget examples we would look at paying down the car loan and the bank loan as quickly as possible, since those are easy wins.

Student debt at an average of 4.3% interest is typically lower interest than these other loans, so is the third priority for us today.

At the same time we still need to save, when im paying down debt aggressively I still always save a minimum of $100 per month. This way I still cultivate the good habit of saving and get a huge confidence boost when I see I’ve saved 4 figures over the course of 12 months.

If I follow my own advice I now have $650 to spend paying down my debt each month.

Once the car and bank loans have gone, my original $750 surplus is mine, to go into savings, starting a business, going on vacation, anything I set my mind to.

The money I’m now saving from not having to pay back car and bank loans, can for example be re-directed to paying down the student loan.

There are lots of variables to this, but this is at its most basic the key to financial freedom, through understanding financial literacy at it most basic level and being able to develop a budget and then an action plan to save and pay off debt with the surplus cash, you make room for in your life.

I see so many people like myself who get consumed with debt, it becomes a never ending cycle but with some simple easy to use tools and a little bit of time, we can create plans to get ourselves out of those situations.

What next?

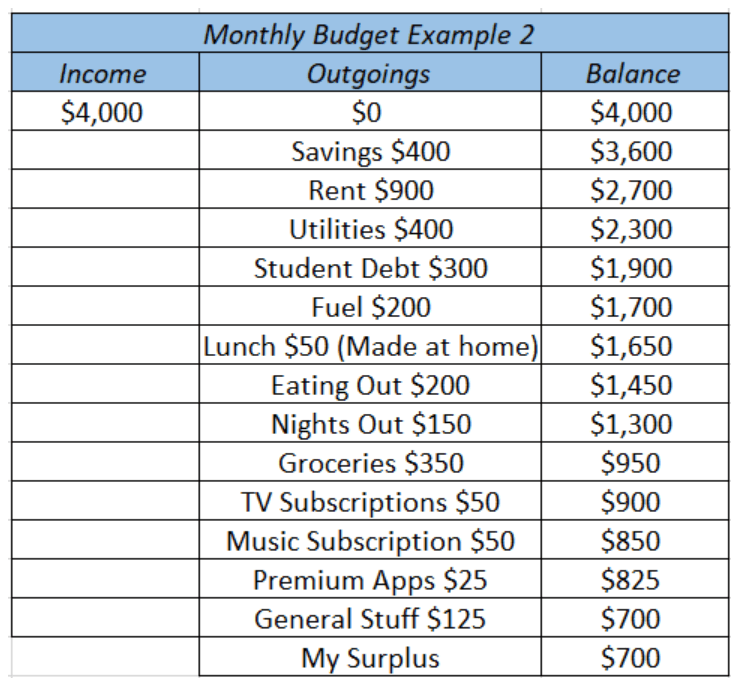

Ok so once that’s done and those high cost debts are eliminated, its time to pivot our thinking and save as literally priority number 1, or what you will hear being called pay yourself first.

The basic idea is that before you do anything else with your income, that a percentage goes straight to savings, generally that would be a minimum of 10%, so if we have paid down the high cost debt, the pay yourself first budget would look like the below:

By paying ,myself first I’ve now saved $400 straight away, it comes automatically into my savings account the day my salary lands so I don’t notice it.

But because I’ve paid down my high cost debt and my expenses are less, I now have $700 in surplus cash each month to do what I want. Which could be anything from saving more, to getting rid of student debt, to investing, to well just buying something if I really want or need to without getting into debt.

Next time I will take a deeper dive into saving strategies and share some hints and tips on how to maximize the potential of your savings.

The top 3resources that have helped my enormously on my own journey so far are:

The Richest Man in Babylon by George S Clason

The Rich Dad, Poor Dad series by Robert T Kiyosaki

Think and Grow Rich by Napoleon Hill

*I am not now and have not been at any time compensated to endorse or advertise these books or the respective authors*